What are Central Banks?

Someone needs to control the money supply

Hope you had a chance to read my previous post about ‘What is Money’, if you haven’t yet, I suggest you to take a quick read here: What is Money The following post is a continuation of the chain of thought on how money works. I am sure you must’ve heard of the name Federal Reserve almost every time you turn on the TV or your financial news source these days. You must be wondering what exactly is a central bank? The Federal Reserve is the central bank of the United States, which is mandated to provide the nation with a safe, flexible, and stable monetary and financial system.

Definition of Central Bank:

A central bank is an institution designed to oversee the country’s banking system and regulate the quantity of money in the economy. Yes, money can be regulated that like any other commodity. Federal Reserve was founded by an act of Congress in 1913, almost more than a 100 years ago now.

Some examples of Central Banks today:

European Central Bank (ECB)

Bank of Japan (BOJ)

Bank of England (BOE)

Bank of Canada (BOC)

US Federal Reserve (FED)

Whenever an economy relies on fiat money, there must be some agency that regulates the quality of the system. With the U.S. dollar used for approximately 85%-90% of all the world's currency transactions, the Fed’s is by far the most powerful and influential central bank. Centrals banks have a lot of functions to take care of (like below):

The Federal Reserve is designed to be independent, but also does its work alongside other institutions that have a role in the nation's economy and banking system, like the Treasury, the Department of Labor, the Federal Deposit Insurance Corporation (FDIC), and more. The Treasury Department is the executive agency responsible for promoting economic prosperity and ensuring the financial security of the United States.

Official role of Treasury:

“The U.S. Department of the Treasury's mission is to maintain a strong economy and create economic and job opportunities by promoting the conditions that enable economic growth and stability at home and abroad, strengthen national security by combating threats and protecting the integrity of the financial system, and manage the U.S. Government’s finances and resources effectively.”

(https://home.treasury.gov/about/general-information/role-of-the-treasury)

How does Central Bank Function:

Central banks affect economic growth by controlling the liquidity in the financial system. They have three monetary policy tools to achieve this goal.

First, they set a reserve requirement. It's the amount of cash that member banks must have on hand each night. The central bank uses it to control how much banks can lend.

Second, they use open market operations to buy and sell securities from member banks. It changes the amount of cash on hand without changing the reserve requirement. They used this tool during the 2008 financial crisis. We will talk about 08 crisis in a separate post.

Third, they set targets on interest rates they charge their member banks. This is the guidance rate used by banks for consumer loans, mortgages, etc.

Since the Fed can influence the availability and cost of money to promote a healthy economy. Congress has given the Fed two co-equal goals for monetary policy:

Maximum employment

Stable prices, meaning low, stable inflation.

This “dual mandate” implies a third, lesser-known goal of moderate long-term interest rates. More generally, maximum employment is a broad-based and inclusive goal that is not directly measurable and is affected by changes in the structure and dynamics of the labor market. So, the Fed doesn’t specify a fixed goal for employment. And recent estimates of the longer-run rate of unemployment that is consistent with maximum employment are generally around 4 percent.

Monetary Policy:

The Fed implements monetary policy primarily by influencing the federal funds rate, the interest rate that financial institutions charge each other for loans in the overnight market for reserves. Changes in the federal funds rate tend to cause changes in other short-term interest rates, which ultimately affect the cost of borrowing for businesses and consumers, the total amount of money and credit in the economy, and employment and inflation. All the major banks in US are required to have a reserve account with the Federal Reserve, which set’s the reserve amount requirement needed. Reserve requirements are the amount of cash that financial institutions must have, in their vaults or at the closest Federal Reserve bank, in line with deposits made by their customers.

To keep price inflation in check, the Fed can use its monetary policy tools to raise the federal funds rate, which can be restrictive or expansionary. Raising interest rates slows growth, preventing inflation. That's known as contractionary monetary policy. Lowering rates stimulates growth, preventing or shortening a recession. That's called expansionary monetary policy. More of this in next section

Implementing Monetary Policy is done primarily using the following:

Reserve Requirements: The Federal Reserve Act of 1913 required all depository institutions to set aside a percentage of their deposits as reserves, to be held either as cash on hand or as account balances at a Reserve Bank. The Act gave the Fed the authority to set that required percentage for all commercial banks, savings banks, savings and loans, credit unions, and U.S. branches.

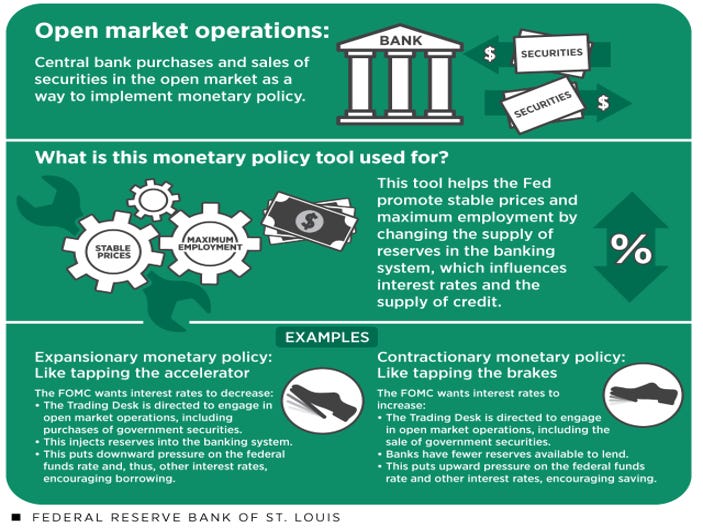

Open Market Operations: This consists of buying and selling U.S. government securities on the open market, with the aim of aligning the federal funds rate with a publicly announced target set by the Federal Open Market Committee (FOMC). The Federal Reserve Bank of New York conducts the Fed’s open market operations through its trading desk.

If the FOMC lowered its target for the federal funds rate, then the trading desk in New York would buy securities on the open market to increase the supply of reserves.

The Fed paid for the securities by crediting the reserve accounts of the banks that sold the securities. Because the Fed added to reserve balances, banks had more reserves that they could then convert into loans, putting more money into circulation in the economy.

In turn, short-term and long-term market interest rates directly or indirectly linked to the federal funds rate also tended to fall. Lower interest rates encourage consumer and business spending, stimulating economic activity and increasing inflationary pressure.

Once implemented, there are two types of Monetary policy that FED will pursue depending on the state of the economy :

Tapping the accelerator: expansionary monetary policy

Policymakers refer to this as “easing” or expansionary monetary policy—pushing on the gas pedal to give the economy more fuel and to encourage economic activity, such as in times of slower employment growth or a potential economic downturn.

Tapping the brakes: contractionary monetary policy

Policymakers call this “tightening” or contractionary monetary policy—tapping the brakes to slow down the car and restrain spending when price stability is at risk due to higher-than-desired inflation

There are much more finer nuances on how exactly the monetary policy is implement and how many other participants are involved but broadly speaking the central banks are tasked to control the money supply through operations in the open market either by tweaking the rates or buying/selling the US debt securities.

M1 and M2 Supply:

Remember we discussed about M1 and M2 in my earlier post. To refresh your memory:

M1 = coins and currency in circulation + checkable (demand) deposit + traveler’s checks.

M2 = M1 + savings deposits + money market funds + certificates of deposit + other time deposits.

The Federal Reserve System is responsible for tracking the amounts of M1 and M2 and prepares a weekly release of information about the money supply. The below chart shows the supply of M1 and M2 over the past years:

In 2020, the Federal Reserve changed the definition of both M1 and M2. The biggest change is that savings moved to be part of M1. M1 money supply now includes cash, checkable (demand) deposits, and savings. M2 money supply is now measured as M1 plus time deposits, certificates of deposits, and money market funds. This led to a massive spike in the chart of M1 which now also includes savings amount. The reason for this is due to change in regulation in 2020.

The Federal Reserve requires banks to hold reserves against checkable deposits. But the regulation does not require banks to hold reserves against savings and money market accounts, which restrict depositors to no more than six transfers or withdrawals per month. These latter accounts are highly liquid (and in the case of some money market funds, even checkable). On April 24, 2020, the Federal Reserve Board announced that Regulation D would no longer impose limits on the number of transactions or withdrawals permitted on savings deposit accounts. According to this ruling, if a bank suspends enforcement of the six-transfer limit on a savings deposit, the bank may report that account as a “transaction account” on its reserve reports. It seems that the modification of Regulation D in late April 2020 has effectively rendered savings accounts almost indistinguishable from checking accounts from the perspective of depositors and banks

In our next post, we will be talking about the banks which work with federal reserve to stimulate the economy and how do they do it using customer deposits. Stay tuned!